When a Malaysian business decides to invest in custom software, the conversation usually goes straight to price. How much does it cost? What's the payment schedule? Can we get a discount? The question that almost never gets asked — but should — is: how should we structure this investment for tax purposes?

The answer has a meaningful impact on your effective cost. Not theoretical. Actual ringgit you either keep or give to LHDN. This article is not tax advice — you should take this to your accountant. But it will give you the right questions to ask before you sign anything.

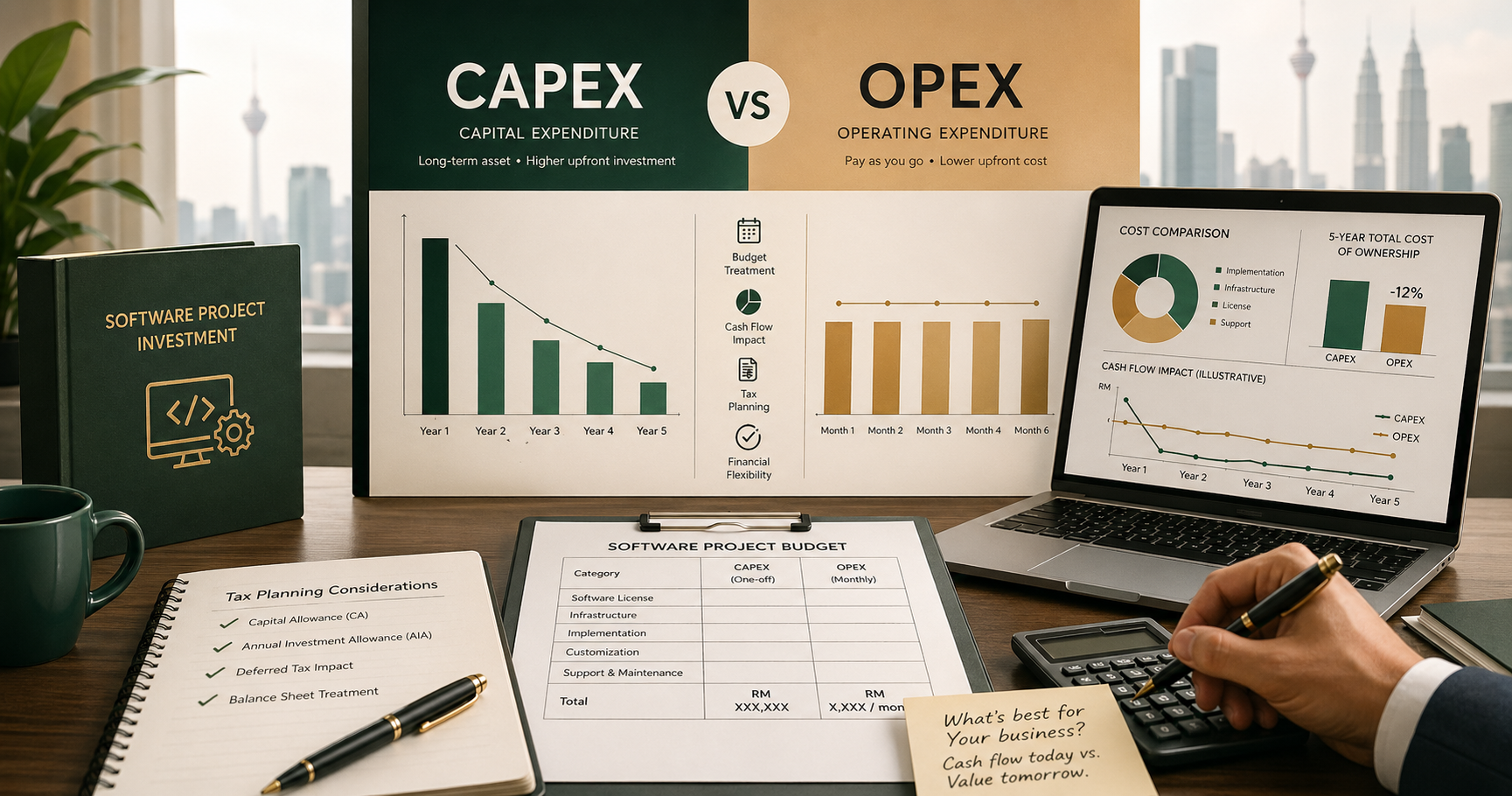

What is CAPEX for software?

CAPEX — Capital Expenditure — means you're treating the software as a long-term asset on your balance sheet. You purchase it, it gets capitalised, and you depreciate it over its useful life.

Under Malaysian tax law, the treatment for computer software and IT systems falls under the Capital Allowance regime. In the first year, you can claim an Initial Allowance plus an Annual Allowance — the combined deduction in Year 1 is typically around 40% of the asset cost. The remaining 60% is spread across subsequent years.

At a 24% corporate tax rate, a CAPEX software investment gives you back approximately 9.6 cents for every ringgit spent in Year 1 as a tax saving. Better than nothing — but not the full picture.

What is OPEX for software?

OPEX — Operating Expenditure — means the software investment is treated as a recurring business expense, not a capital asset. Instead of buying a system outright in milestone payments, you pay a fixed monthly fee over a defined period under a managed service agreement.

The critical difference: operating expenses are 100% deductible in the year they're incurred. Every ringgit you spend is deductible against your taxable income in that financial year.

At a 24% corporate tax rate, a fully OPEX-structured software investment gives you back 24 cents for every ringgit spent in Year 1. That's 2.5 times the tax recovery of the CAPEX approach — in the same financial year.

The tax difference — a worked example

Consider any significant software project. Under CAPEX at a 24% corporate tax rate, you recover approximately 40% as a tax deduction in Year 1 — the rest is spread over future years. Under OPEX, the entire investment is deductible in Year 1, giving you 100% recovery at your applicable tax rate. The effective cost difference between the two models — on the same project, at the same price — can be substantial. On larger enterprise projects, this difference runs into tens of thousands of ringgit.

This is why, at Trendtive Digital, we always present both models to clients and let them choose with full information. Many clients — once they see the comparison — opt for OPEX. Some don't, and that's a legitimate choice depending on their specific cash flow and balance sheet needs. But everyone deserves to make that choice consciously.

Why most Malaysian businesses default to CAPEX

It's largely familiarity. Procurement teams are used to raising purchase orders. Finance teams are used to capitalising software. Accountants default to asset classification when something costs a significant amount and has a multi-year useful life.

Most agencies don't raise this topic because they're not advisors — they're vendors. Their job is to close the sale, not to optimise the client's tax position. The CAPEX vs OPEX question gets missed not because it's complicated, but because no one in the room is incentivised to raise it.

"Most agencies don't raise this topic because they're vendors, not advisors. The question gets missed not because it's complicated, but because no one in the room is incentivised to raise it."

When CAPEX might actually be the right choice

This isn't a one-size-fits-all recommendation. There are legitimate reasons to prefer CAPEX for a software investment:

- You want the asset on your balance sheet. Some businesses — particularly those seeking financing or preparing for acquisition — benefit from showing capitalised software assets.

- Your cash flow strongly favours milestone payments over monthly fees. Some businesses find it easier to budget large milestone payments tied to delivery events than a fixed monthly commitment.

- Your corporate tax rate is low or you're in a loss position. If you're not generating significant taxable profit, the tax deductibility advantage of OPEX is less meaningful in the near term.

- The project has an unusually long and definable useful life. If the system will genuinely be used for 10+ years with minimal change, spreading the capital allowance makes financial sense.

What to ask your vendor before you sign

Before committing to either model, these are the four questions worth putting to any software vendor:

-

1Can this project be structured as a managed service? If the vendor only offers milestone-based purchase contracts, OPEX may not be available. A vendor who offers monthly fixed-fee delivery with a defined project end date enables OPEX classification.

-

2Will I receive monthly invoices I can expense as operating costs? The invoice structure matters for your accountant's treatment. Monthly service invoices are operationally expensed. A single large invoice or milestone-based invoice is typically capitalised.

-

3Is source code ownership transferred at project close regardless of model? Under a managed service, you're paying monthly — but you should still own everything at the end. Confirm that IP transfer is unconditional and not contingent on future payments beyond the agreed term.

-

4What's the warranty and support arrangement under each model? Some vendors bundle support into the OPEX model that would cost extra under CAPEX. Get a clear comparison of what's included under both structures — not just the tax implications.

The conversation worth having

None of this is a reason to choose one agency over another. It's a reason to have a more complete conversation before you decide. The best time to raise the CAPEX vs OPEX question is before the proposal is issued — not after the contract is signed.

Take these questions to your accountant alongside the vendor's proposal. Ask them to model the Year 1 tax impact under both scenarios using your actual corporate tax rate. The answer will either confirm your default approach or give you a compelling reason to ask your vendor for an alternative structure.

Either way, you'll be making the decision with full information — which is the only way this kind of decision should be made.

This article provides general information only and does not constitute tax or financial advice. Consult a qualified tax advisor regarding your specific circumstances before making any investment structuring decisions.